Get Your 100% Free

Debt Relief Consult

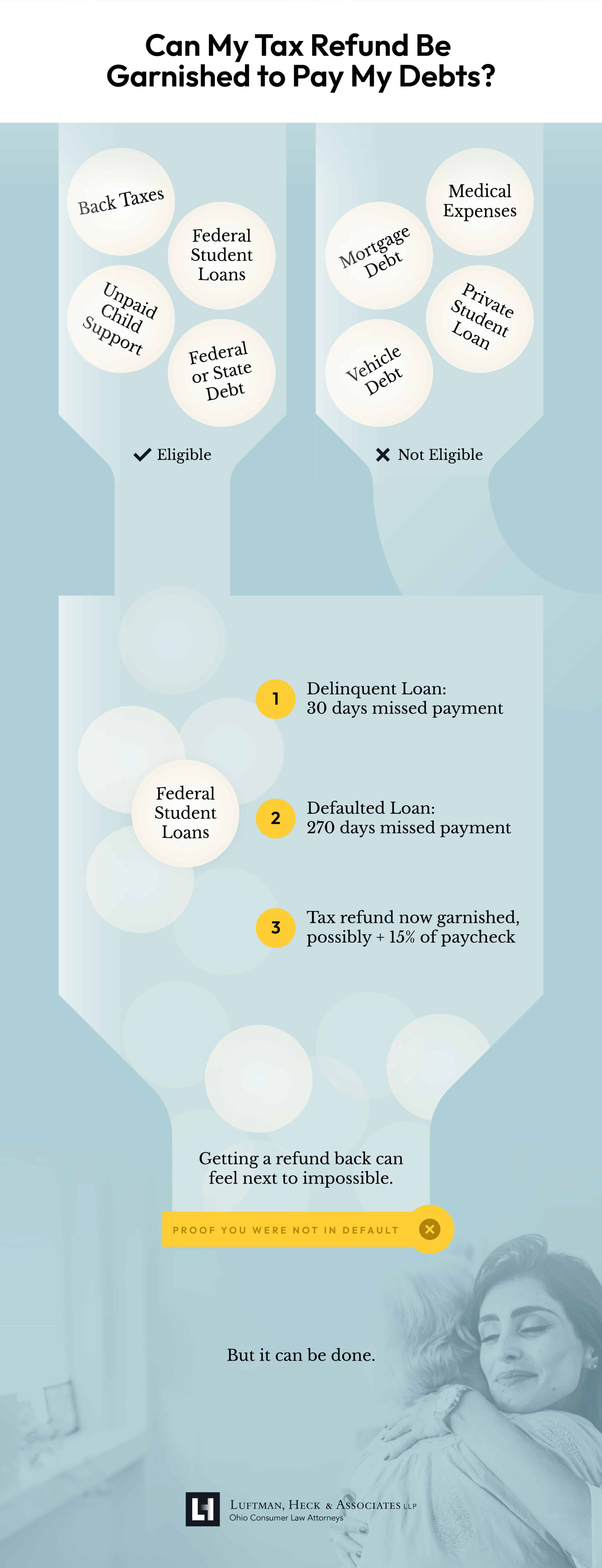

Can My Tax Refund Be Garnished to Pay My Debts?

For many, their annual tax refund delivers a critical financial boost, aiding in everything from vacation plans to paying bills. Yet, the shadow of tax refund garnishment looms if you’re struggling with outstanding debts, particularly when their debts are owed to or backed by the government.

However, by understanding tax refund garnishment and exploring debt strategies to prevent it are helpful ways to maintain your financial health.

What Debts Can Lead to Tax Refund Garnishment?

Unlike traditional garnishment, tax refund garnishment doesn’t apply to all types of debt. The IRS and state governments typically enforce it for specific obligations, including:

- Back taxes

- Federal student loans

- Unpaid child support

- Debts to federal or state governments (Workers’ compensation premiums, Ohio Job & Family Services, etc)

Importantly, private debts like mortgages, auto loans, and medical bills do not directly trigger tax refund garnishment. However, once your refund hits your bank account, it becomes fair game for private creditors through legal channels.

How are Tax Refunds Garnished?

The Treasury Offset Program (TOP) is the primary tool for garnishing federal tax refunds, targeting debts to government entities. Similarly, Ohio’s state tax refund garnishment program mirrors the federal approach, applying to state and federal tax debts, Attorney General’s office debts, and certain state-administered obligations.

When the Ohio government garnishes your state tax refund, they will send you a letter explaining why you were subjected to offset, and which government agency was owed money. If the Ohio government is unable to recover everything you owe, it may file a request with the TOP in the hopes of garnishing your federal tax refund too.

Can Tax Refunds Be Garnished to Pay Student Loan Debt?

Tax refund garnishment is a real issue for those struggling with student debt. And while the government can only garnish your tax refund if you have defaulted on a student loan, this applies to many Ohioans.

When you miss a loan payment by more than 30 days, your student loan becomes delinquent. If you fail to make a payment after 270 days, the loan goes into default, at this point, your tax refund may be garnished.

Although your loan servicer must provide you with notice of their intent to seek a tax offset, a failure to receive notice is not a basis for challenging the garnishment of your tax refund. If your tax refund is insufficient to pay back the delinquent portion of your loan, they may also garnish up to 15 percent of your wages.

Can I Get My Refund Back if it Was Garnished?

It is very difficult to contest tax offsets. You may request a hearing to contest the garnishment but to prevail, you will need to demonstrate that you were not in default on your debt. But in most cases, borrowers who are subjected to a tax refund garnishment are in fact, in default on their debt.

If you are married and file your taxes jointly, you may have had your tax refund garnished because of your spouse’s debt. In such cases, you may be able to get your portion of the refund back by filing an “injured spouse claim” with the IRS. You will need to demonstrate that the tax offset occurred because of your spouse’s debts and that the debts in question were solely theirs.

How to Avoid Tax Refund Garnishment

Falling into debt can feel overwhelming, but you are not alone, and there are strategies to prevent garnishment and protect your financial resources. Two possible strategies involve Income-Driven Repayment Plans for federal student loans and considering filing for Chapter 7 or Chapter 13 bankruptcy in more severe debt situations.

Each strategy serves a unique purpose in managing and mitigating debt, but it’s essential to understand their nuances and implications, often necessitating the guidance of a skilled debt attorney.

Income-Driven Repayment Plans (IDR)

For individuals grappling with federal student loans, enrolling in an Income-Driven Repayment Plan offers a viable solution to prevent default—a primary cause of tax refund garnishment. IDR plans calculate your monthly payment based on your income and family size, making your student loan debt more manageable and less likely to spiral into default.

Benefits of IDR:

When debts become overwhelming, Chapter 13 and Chapter 7 bankruptcy emerge as viable strategies. By restructuring debts into a manageable repayment plan, Chapter 13 can stop garnishment and other collection efforts, offering a path to financial recovery. Chapter 7 allows you to discharge much of your existing debt and halts collections and garnishments but involves selling (liquidating) nonexempt property and distributing proceeds to creditors. Keep in mind both bankruptcy options involve a legal process to reorganize or eliminate debts, requiring detailed documentation and court approval. Additionally, filing for bankruptcy has a profound impact on your credit score and financial reputation, with long-term implications. These options are by no means you only avenues for avoiding tax return garnishment and dealing with insurmountable debt. That’s’ where an experienced debt and consumer law attorney can help. An experienced and licensed debt attorney can offer strategic advice tailored to your unique financial landscape, help secure your assets, review other debt relief options like lawsuits against creditors for FCRA and FDCPA violations, and pave the way for a more stable financial future where future tax returns are not at risk. Tax Day is almost here. But at Luftman, Heck & Associates, our debt management lawyers, we take pride in our ability to help Ohioans overcome their debt issues. Proper planning, knowledge of your rights, and in some cases, legal action, can remove the cloud of debt over your life. Don’t wait for your loans to go into default before acting. If you are worried that you cannot meet your debt obligations, an Ohio debt lawyer at LHA can help. Jeremiah E. Heck is a leading consumer attorney and founding partner of Luftman, Heck & Associates, committed to helping individuals navigate the complexities of challenging debt. Contact LHA for a 100% free one-on-one consultation.

Consider Bankruptcy

Consult a Debt Relief Attorney

Worried about Your Debt & Tax Refund? Contact LHA Today